What the hell is a 'payments stack'?

What the hell is a 'payments stack'?

A primer on jargon in the payments industry.

Key takeaways

A payment stack refers to the collective set of infrastructure and services that enable customers to make in-store and online payments

The intermediaries that sit between the customer and merchant can be broken down into two groups: (1) issuing parties, which act on behalf of the customer, and (2) acquiring parties, which act on behalf of the merchant

The key parties are the issuing bank (i.e. the customer’s bank), the acquiring bank (i.e. the merchant’s bank), and the card network (e.g. Visa, Mastercard)

Payment gateways and payment processors facilitate transactions by processing transactions and providing other value-added services to issuing banks and merchant acquirers

A payment is comprised of three distinct processes: authorisation, reconciliation and settlement—which collectively accrue fees totalling 2-3% of the amount transacted

So far, technology-enabled innovations in the payments space have been concentrated around the merchant acquiring side of the payments stack

Nowadays, anything moderately tech-enabled seems to be shrouded in a maze of buzz-words and industry jargon. In my journey to better understand the payments ecosystem, I wanted to cut through the noise by breaking down the concept of the payments stack—a term used to refer to the collective set of infrastructure and services that enable customers to make payments with merchants in-store and online.

Ecosystem players

From the perspective of a customer, the payments process may seem deceptively simple—you simply swipe a card and the cost of the item you are purchasing is immediately debited from your account. But beneath the surface of that card swipe is a complex series of procedures, facilitated by network of intermediaries, each fulfilling a specific function within the transaction process.

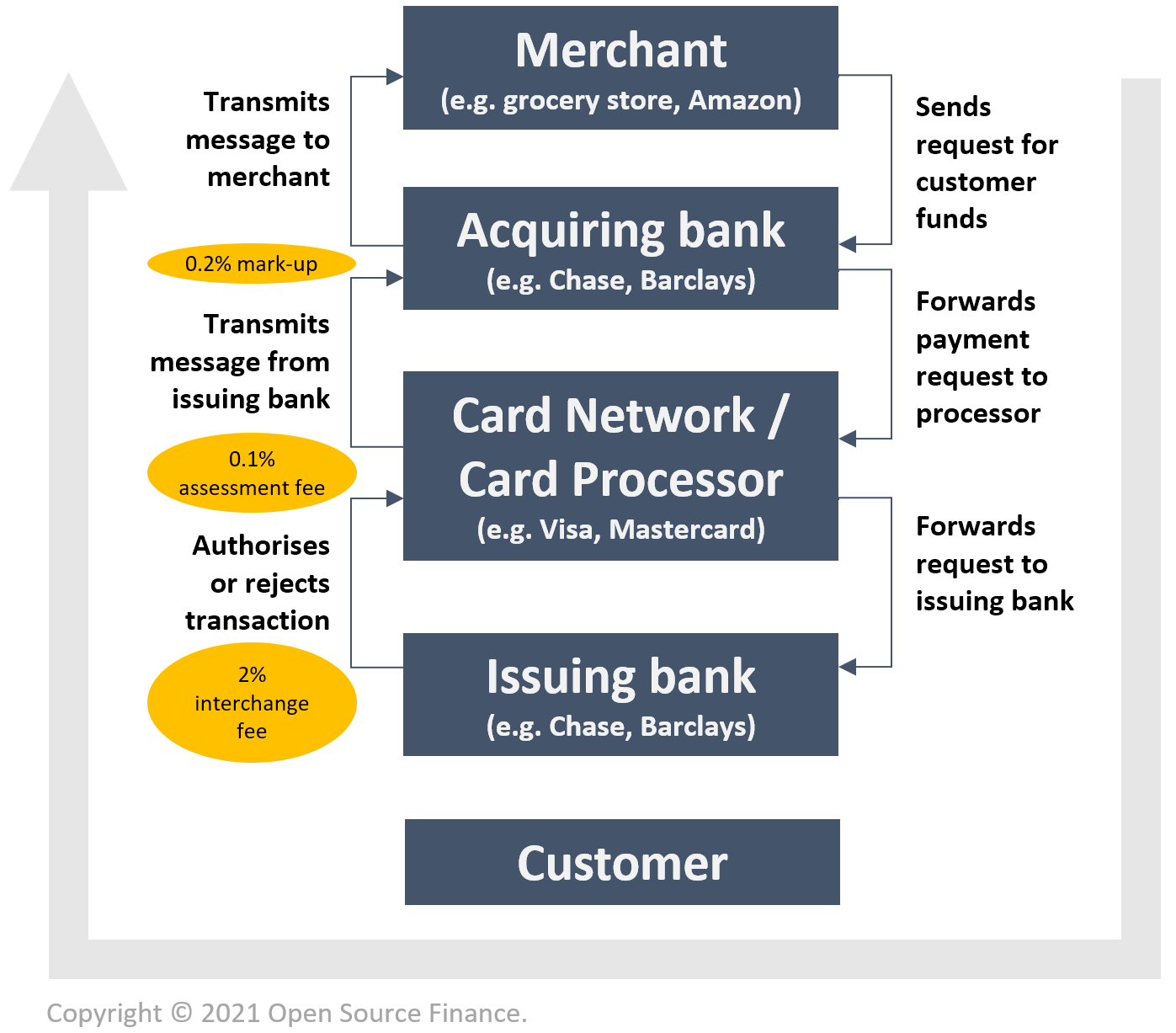

The figure below identifies these counterparties and the services they provide.

In the traditional payments ecosystem, the customer and merchant are connected via a card network (e.g. Visa, Mastercard), which provides the infrastructure for processing payments. The remaining intermediaries sit between the card network and customer / merchant respectively and can be divided between:

the issuing side, which acts on behalf of the customer. In particular, the issuing bank issues credit and debit cards to customers which allow them to make payments (sometimes on credit).

the acquiring side, which acts on behalf of the merchant. The acquiring bank acquires merchants by allowing them to accept payments on the card network.

There are other intermediaries that provide payment processing and other value-added services across the payments value chain. For instance:

a payment service provider (PSP) / payment gateway aggregates different payment methods to provide a seamless user experience at the point of sale (see screenshot below). PSPs also increasingly provide transaction encryption, embedded payment forms and other merchant-facing services on the back end.

an issuing processor ensures compliance and provides fraud detection and other services, acting as an intermediary between the issuing bank and the card network.

We’ve covered a lot of players so far. By way of summary, the key parties to the payments ecosystem (setting aside the customer and merchant) are:

the issuing bank, which acts on behalf of the customer

the card network, and

the acquiring bank, which acts on behalf of the merchant.

Typical payment cycle

When you swipe your card at a checkout counter (or checkout online), the merchant’s bank sends a message to your bank to verify that you have adequate funds in your account. The transaction is then either authorised or rejected, and if the former, funds are transferred via the card network to the merchant bank.

This process (called a payment cycle) is broken down into three steps:

Authorisation: at the point of sale (e.g. when you swipe your card), a request is sent from the merchant to the customer’s issuing bank to check for availability of funds and authorise the transaction. This request is passed along all the way through the payments stack.

Clearing: periodically (e.g. at the end of each business day), merchants send information about all transactions to their acquiring bank for reconciliation, and to ensure everything has been properly accounted for.

Settlement: finally, money is transferred from the customer’s issuing bank to the merchant, again working its way through the entire payments stack..

A typical payment authorisation process (based on this explanation). The transaction fees shown are illustrative.

At each step of the payments process, intermediaries takes a cut for the services they provide. These fees tend to sum to around 2-3%, and include:

a non-negotiable interchange fee charged by the issuing bank, typically of around 2%. Issuing banks tend to retain the largest cut of fees because they incur significant variable and customer acquisition costs.

a non-negotiable assessment fee charged by the card network, typically of around 0.1%. Card networks deal in high volume so even though they capture a relatively low proportion of fees, the amount they accrue is significant when scaled across a large number of transactions.

a negotiable mark-up charged by the acquiring bank (or other payment processors or payment gateways used by the merchant), typically of around 0.2%.

The fees shown above are only illustrative, and actual fees are likely formed of a mix of fixed and variable rates, potentially with tiered pricing and even subscription-based models.

Evolution of the payments stack

With the proliferation of online and mobile payments, the merchant acquiring side of the business has seen significant transformation over the past decade. Companies like PayPal and Stripe are disrupting this part of the stack by building integrated payment gateway and processing platforms that not only allow merchants to accept a wider range of payment methods, but also provide essential services like PCI compliance, payment APIs, webhooks and chargebacks that help meet the complex needs of today’s e-commerce titans.

As online marketplaces grows in size and complexity, the payments industry will likely need to continue to evolve to meet the demands of merchants. Viable alternatives are cropping up in the form of Alternative Payment Methods (APMs) like Google Pay and cryptocurrencies like Bitcoin, the latter of which completely replaces the traditional payments stack. It would be interesting to see how the sector continues to grow and evolve in the light of the shifting needs of their customers and mounting competitive pressures.

Subscribe to the blog

Hi, I’m Park!

Open Source Finance is a blog to document my journey into the complex and fast-moving world of fintech. In this blog, I share ideas, insights and key learnings about companies, technology, entrepreneurship, innovation and more.

Finance is better when it’s open source. If you enjoy Open Source Finance, please consider subscribing and sharing it with your social network to help me build my profile!