Coinbase Deep-dive and Investment Thesis: Part 1

Coinbase Deep-dive and Investment Thesis: Part 1

The company's mission, the problem it solves, its competitive position, and the key risks to Coinbase's business.

Disclaimer: The information and views expressed in this article are those of the author only and intended for educational purposes. They do not constitute any form of advice or recommendation to be relied upon in making (or refraining from making) investment decisions.

Key takeaways

Coinbase’s mission is to become the most trusted and easy-to-use provider of financial services in the cryptoeconomy.

Coinbase removes friction in two ways, by abstracting away the technical complexity of interacting with the blockchain (simplifying use) and acting as a trusted intermediary (providing trust).

Coinbase has built a strong reputation as one of the most user-friendly and trusted exchanges in the US, but it faces substantial competition abroad and from alternative on-ramps to the cryptoeconomy.

Most of the revenues generated by Coinbase today derive from transaction fees charged on the exchange of crypto assets, particularly by retail customers. This makes Coinbase highly exposed to market volatility in terms of asset prices. It is also subject to fee competition over the longer term.

To mitigate these risks, Coinbase will need to scale its institutional business and transform its revenue structure—by moving away from transaction-based revenues and toward monetising its asset base.

Earlier this month, Coinbase completed the direct listing1 of its Class A common shares, ushering in a new era for crypto and solidifying its legitimacy within traditional finance spheres.

I have been a user of Coinbase since 2017. It was my first on-ramp to the cryptoeconomy, at a time when not many options existed. I still remember opening the Coinbase app after work every day to buy crypto (the purchase limits refreshed every hour or so, and by day’s end I would have another £50 or so in my allocation). Since then, Coinbase has evolved into an ecosystem of services that facilitates broad access to the cryptoeconomy for retail investors, institutions and merchants alike.

In this three-part series, I do a deep dive into Coinbase’s business and present my investment thesis for the company. My analysis has been enabled in large part by the S-1 form2 filed by Coinbase with the SEC this February, which contains a detailed overview of Coinbase’s business, its financial position, and other useful information. As a financial analyst, I was naturally curious to dissect that document and understand more about the company:

in this first part, I review the business case for Coinbase. I try to understand its mission, the problem it solves, its competitive position, and the key risks to its business.

in Part 2, I conduct a financial and operational review of the company, looking at the build-up of its revenues, key drivers and its cost structure.

in Part 3, I attempt to value the company using conventional valuation methods. I set out my investment thesis for Coinbase and close with some thoughts for the future.

If you are already familiar with Coinbase, please feel free to skip ahead using the links provided above.

Purpose and mission

Coinbase’s goal is to become the most trusted and easy-to-use provider of financial services in the cryptoeconomy, allowing anyone to buy, sell, spend, save and earn in cryptocurrency.

In doing so, its mission is to reduce the frictions associated with participating in the cryptoeconomy and build a fairer, decentralised and more transparent financial system.

Product

Coinbase was founded in June 2012 by Brian Armstrong. The company first launched its service to allow customers to buy and sell Bitcoin through bank transfers in October 2012. It has since launched several other products as part of a comprehensive, full-stack offering:

Coinbase: a retail-focused product that allows users to buy, sell and store cryptocurrencies

Coinbase Pro: a trading product targeted toward professional traders

Coinbase Wallet: a mobile application that allows users to access decentralised applications built on Ethereum and other blockchains

Coinbase Card: a debit Visa card that allows customers to spend their cryptocurrency

USD Coin (USDC): a digital stablecoin launched as part of a consortium comprising other investors called Centre

Coinbase Prime: a prime brokerage platform for institutional investors

Coinbase Custody: a custodian service with dedicated cold storage solution for institutional investors

Coinbase Commerce: a service that allows merchants and payment service providers to accept cryptocurrency payments

Value proposition

Coinbase serves as a crucial on-ramp for retail investors, institutional investors and e-commerce partners seeking to participate in the cryptoeconomy. It does so by providing the necessary infrastructure to allow for frictionless participation, in two ways:

by abstracting away the technical complexity of interacting with the blockchain (i.e. simplifying use). Coinbase has achieved this by re-investing heavily in technology and building out its suite of products.

by acting as a trusted intermediary to which users can delegate their assets (i.e. providing trust). It continues to seek regulatory compliance and consumer protections across the geographies in which it operates.

Most of the revenues generated by Coinbase today derive from transaction fees charged on the purchase and sale of crypto assets, particularly by retail customers. This is a substantial and growing market, but is likely exposed to volatility across the market cycle and, more importantly, fee competition from other service providers.

To offset this risk, Coinbase has continued to invest in its institutional product offering and other services that generate recurring revenues. The ability of Coinbase to scale its revenues over the long term will depend on whether it is able to transition away from short-term trading activities (i.e. fees earned on transaction volumes) and toward long-term investment activities (i.e. fees charged on assets under its management) and its recurring revenue businesses.

There are emerging opportunities, for instance in the Proof-of-Stake consensus and DeFi space, that could shift the focus of users towards investing for the long term. These could present interesting revenue opportunities for Coinbase.

Addressable market

The addressable market for Coinbase is tied to the wider adoption of cryptocurrencies and the demand for crypto-based financial services. Today, Coinbase serves over 43 million retail users and 7000 institutions, and it is likely that these numbers will continue to grow. A 2020 survey conducted by Statista found that only 6% of US respondents had ever used or owned cryptocurrencies. That proportion is higher in countries like Nigeria and the Phillipines where existing payment rails are weak, but even there the scope for continued adoption remains significant.

Coinbase’s aspiration is to “bring crypto-based financial services to anyone with a smartphone, a population of approximately 3.5 billion people today”.3 With its range of products catered to both new and sophisticated users, Coinbase has the unique opportunity to take on a massive and rapidly growing market.

Of course, there are risks to adoption which could lead to a narrowing of the addressable market. I discuss these and other risks in more detail below.

Competitive position

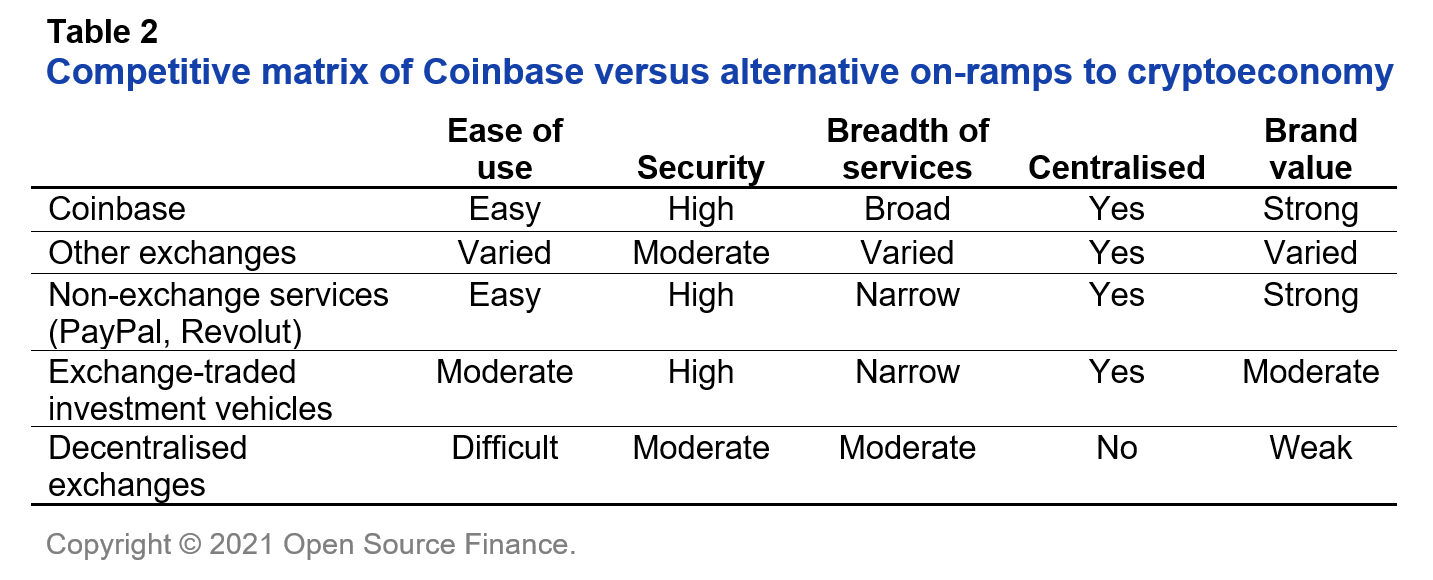

Coinbase has built a strong reputation as one of the most user-friendly and trusted exchanges in the US, but it faces substantial competition from rival exchanges and alternative on-ramps to the cryptoeconomy.

As shown above, Coinbase leads the US market in terms of its popularity, despite having support for relatively few cryptocurrencies. This speaks to the strong brand value and customer relationships it has maintained in the market. The international market is larger and dominated by Binance, which leads on liquidity, popularity and the breadth of its product offering.

Other non-exchange services like PayPal and Cash App in the US and Revolut in the UK have gradually added cryptocurrency offerings, which compete against Coinbase as alternative on-ramps to the crypto market. Investment vehicles like the Grayscale Bitcoin Trust and other Bitcoin ETFs also provide alternative avenues for retail and institutional investors to invest in crypto. That said, some of these providers are likely to be clients of Coinbase (for instance, Grayscale Investments relies on Coinbase’s institutional brokerage product to provide its asset management services). This creates synergistic opportunities for revenue capture, offseting some of the competitive risk.

Lastly, Coinbase competes against the ecosystem of decentralised exchanges that have come onto the market recently, including Automated Market Maker (AMM) based exchanges which are noncustodial and offer alternative investment products such as liquidity pools.

Despite the threat of competition, Coinbase has built important competitive advantages that allow it to maintain its market leading position. It continues to hold the largest share of total crypto market capitalisation on its platform. Coinbase’s key competitive advantages include:

regulation and compliance: Coinbase is a regulated entity and has obtained licences to operate in most US states, as well as countries internationally. It complies with customer due diligence / anti-money laundering regulation, reporting requirements and other laws and regulations in the US.

insurance and security: Coinbase holds the majority of its crypto asset deposits in cold storage and has secured insurance over the full value of these assets. It has never been the subject of a security breach.

investment in technology: Coinbase has continued to expand its service offerings and integrate a growing ecosystem of blockchains, while maintaining the simple, intuitive UX layer that it is known for.

service offering: Coinbase has built innovative products and created a differentiated service offering, for instance focusing on products that promote financial education.

partnerships: Coinbase has partnered extensively with merchants, asset issuers, developers and other stakeholders to build its ecosystem of services and create lasting moats.

The figure below attempts to summarise the competitive matrix for Coinbase, in light of the service offerings discussed above.

Risks

As a business that generates most of its revenues from transactions in crypto assets, Coinbase is exposed to significant market risk in terms of the price volatility of assets traded on its platform. In the next part, I will discuss how asset price volatility is an important driver of both Monthly Transacting Users (MTUs) (which drive transaction revenues) and Assets on Platform (which drive subscription-based revenues).

Coinbase also faces the risk of external competition from alternative on-ramps to the cryptoeconomy, as already discussed. The transaction fees that Coinbase is able to charge its retail customers will likely erode over time as competitors grow their service offerings and consumers become more price sensitive.

In particular, crypto purchases made on Coinbase are charged a base transaction fee of 4%, with various reductions depending on payment method and location. Retail users are further charged:

a 0.5% spread on the quoted price of crypto assets, and

a ‘Coinbase Fee’ that varies by order size and region. For example, in the US, the Coinbase Fee ranges from $0.99 for transactions worth $10 to $2.99 for transactions worth between $50 and $200.

This two-tiered model is most likely unsustainable over the long-term as it becomes subject to: (1) internal competition from Coinbase’s Pro product, which can be accessed at no further charge; and (2) external fee competition from other exchange providers.

Brian Armstrong has recently acknowledged that competition could result in “fee compression” over the long-term.

In terms of diversifying its market exposure, Coinbase faces substantial risk in terms of its ability to scale its institutional business and generate recurring revenues. While Brian Armstrong expressed his aspiration for Coinbase to derive 50% of its revenues from its non-trading businesses in five to ten years’ time, this remains speculative as Coinbase’s subscription and service-based revenues are currently subscale. To transform its revenue structure, Coinbase will need to not only influence the behaviours of its customers, but also reinvent itself as more than just an asset exchange.

Of course, there is also the risk that crypto assets will not be widely adopted enough to allow Coinbase to continue to scale its business. Setting aside a black swan event, there are a number of technical, governance-related and regulatory risks that could foreseeably affect the level of adoption of cryptocurrencies. Some of these are idiosyncratic risks specific to each project / blockchain protocol. Maintaining a broad portfolio of crypto assets will allow Coinbase to diversify its exposure.

In the next part, we dive into a financial and operational review of Coinbase and look at the build-up of its revenues, key drivers and its cost structure. I’ll see you there!

Subscribe to the blog

Hi, I’m Park!

Open Source Finance is a blog to document my journey into the complex and fast-moving world of fintech. In this blog, I share ideas, insights and key learnings about companies, technology, entrepreneurship, innovation and more.

Finance is better when it’s open source. If you enjoy Open Source Finance, please consider subscribing and sharing it with your social network to help me build my profile!

The fact that Coinbase chose to pursue a direct listing as opposed to a more traditional Initial Public Offering (IPO) seems like a suitable nod toward its ethos of decentralisation. In short, it avoided the expensive underwriting process (most often brokered by a group of investment banks) and allowed more investors to purchase Coinbase shares upon listing.

I rely on the amended version of the S-1 Form, filed on 23 March 2021.

Coinbase Form S1/A (Amendment No. 2): page 6

👌👌